.png)

.HEIC.jpg)

So you've decided the get a health insurance policy for your company?

Great, your employees will thank you for it!

What next?

These are the questions you need to answer to take the right policy

- What policy terms should you go for?

- How to ensure there are no hidden clauses?

- Which insurer should you go with?

- How do you trust that claims of your employees are honored and serviced on time?

- How do you ensure you're getting the right price for your policy?

1. What policy terms should you go for?

The five most important policy terms that you need to take a call on are

- Family definition: (Self) or (Self + Spouse + Children) or (Self + Spouse + Children + Parents)

- Sum Insured: Typically between 3-5 Lakhs

- Room-rent limits: Typically between INR 3,000 - 10,000 or no-room rent limits

- Maternity limit: Typically covered up to INR 25-50,000; You can choose not to provide this

We've also included some policy benchmarks from other companies here for your comparison

Apart from the above, there are some policy terms you should ensure are checked by default. Many sellers will exclude pre-existing disease coverage or have waiting periods which you need to be careful of

- Pre-existing diseases - Should be covered

- 30 day / 2 year / 4 year waiting periods - Should be waived off

Pre-existing disease coverage is one of the major advantages of a group health policy over individual health policies and ensure that this is covered.

Now you need to make trade-offs between your policy terms and pricing.

2. How to ensure there are no hidden clauses?

Now that you have decided on your policy terms let's look at how to ensure there are no hidden clauses.

The most common hidden clauses are the following

- Low room rent limits: Often times a company offer a high sum-insured of say 7-10L but the room rent limits would be capped at 3,000. This defeats the whole purpose of taking a higher sum-insured. When your room-rent limit is capped at 3,000 any expenses in hospital rooms with a higher per day rent will also be capped no matter what your sum-insured is. To understand what the room rent limits are look for clauses like these

- 1% of sum-insured for regular room and 2% of sum-insured for ICU room

- 2% of sum-insured upto Rs 7000 for regular room

- 5,000 for regular room and 10,000 for ICU room

- Pre-existing diseases are not being covered

The primary advantage of a group health policy is that pre-existing diseases are covered from day one. Many sellers, in order to give you a lower price would insert this clause. Be very careful of it. The most common argument for having this clause inserted is that the population is a young and healthy demographic and hence pre-existing diseases need not be covered. If you're having this clause, just make sure you're making an informed choice about it. - 30 day / 2 year /4 year waiting periods are applied

This clause goes hand-in-hand with pre-existing diseases not being covered. In retail policies there are waiting periods of 2-4 years for many common illnesses. This is a way for insurers to reduce risk and prevent adverse selection. However in a group policy because a larger number of people are insured, this clause is removed in most cases and you should insist on the same.

3. Which insurer should you go with?

When deciding which insurer to pick, you need to look at a few data-points like cashless hospital network, reviews of the insurer from others, claims settlement ratio, claim settlement time, how many claims they have experiencing processing, how fast are their internal processes.

At Nova, we've preselected insurer's for you so you don't have to worry about finding this information yourself.

4. How do you trust that claims of your employees are honored and serviced on time?

When I first started Nova Benefits, I was skeptical that perhaps insurance companies did not have the right intention to make claims. On digging deeper I realized they have the right intentions, but often their processes are not in place or are broken.

For example these are some of the problems that are still unsolved by insurance companies

- responding to an employee's query with a swift turn-around-time

- providing a view to track status of claims at the fingertips of an employee or HR

- being able to assist employees in filling the claim form and filing the claim

- insurer's also raise queries at the time of claims, which an employee does not have expertise in responding to

This is why you need a trusted intermediary or insurance broker to help the employees at time of need and working with an insurer directly can create the above problems. Now to select the intermediary, taking references from past clients is the best way. Ask the intermediary to share testimonials and reference and speak to those folks. Understand how many claims they've had and how helpful was the intermediary with the same. Ask the intermediary if they have a separate claims team, what is their process for assisting employees at the time of claims, what is their claim escalation process, can you see all claims in a single place along with their status

5. How do you ensure you're getting the right price for your policy?

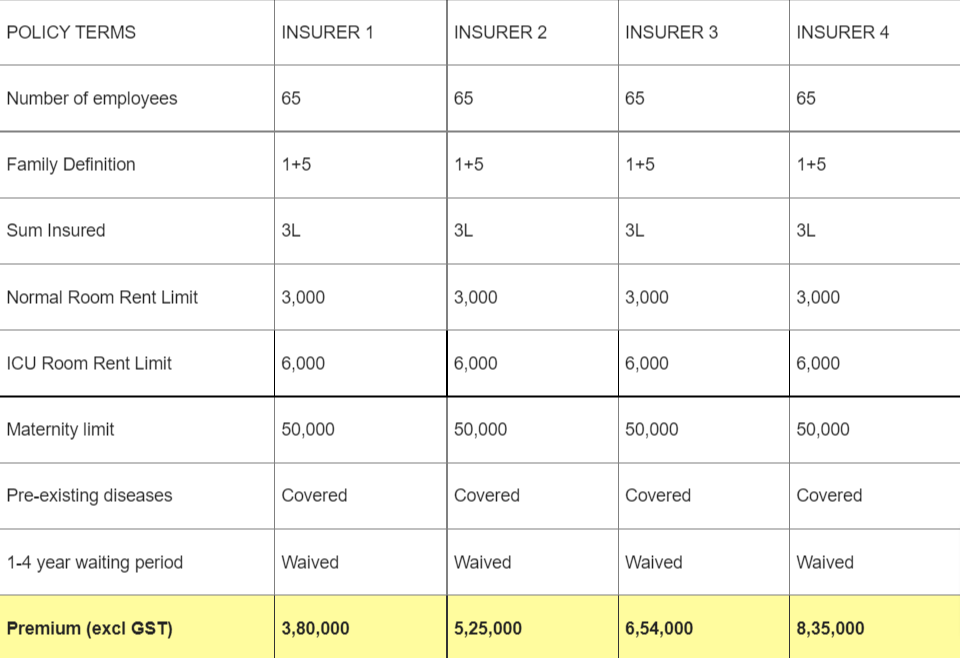

Once you've selected the right policy terms, you want to get quotes from multiple insures. Don't trust the first quote you get, group health insurance pricing is very opaque and the price difference between insurers can be huge. See a quote-sheet below for example

This data is from an actual quote. There is a 40% difference in price between the first insurer and second insurer quote

And even from the same insurer, there is usually some room to negotiate.

Now the down-side of this approach is that is usually very time consuming and there are 25+ insurers in the market. So knowing which ones will give you the right advise on policy terms, the best price and assurance of service quality is tricky.

To save yourself the hassle, go through a trusted intermediary who you know will give you

- the fair & transparent pricing

- give you the best advise

- will take care of your claims

..so that you can focus on your work! Reach out to us to ensure that you invest in the best group health insurance for your team.

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)